Category: Finances

-

Credit Card Service Tax Waiver

I got a call from UOB Credit Card center, they are willing to waive the RM50 service tax off my cards. Condition is I have to pay my telekom (phone) & tenaga (electricity) with it. Or choose 2 of the listed merchants. They need me to fill up the form to do that.

I was about to cancel my cards with them but with this offer, I thought I wait. If I knew earlier, I would not have pull out my insurance payment. By the way, the insurance payment is more than my phone & electricity bill put together. Who cares? As long as I don’t have to pay anything with it.

I have been loyal with UOB for more than 10 years and it is so hard for me to leave home without it. Kudos to them. Now I am waiting for CIMB to make me an offer. If not, it will be goodbye for them.

Let me know if you know of any credit card that provides a service tax waiver.

-

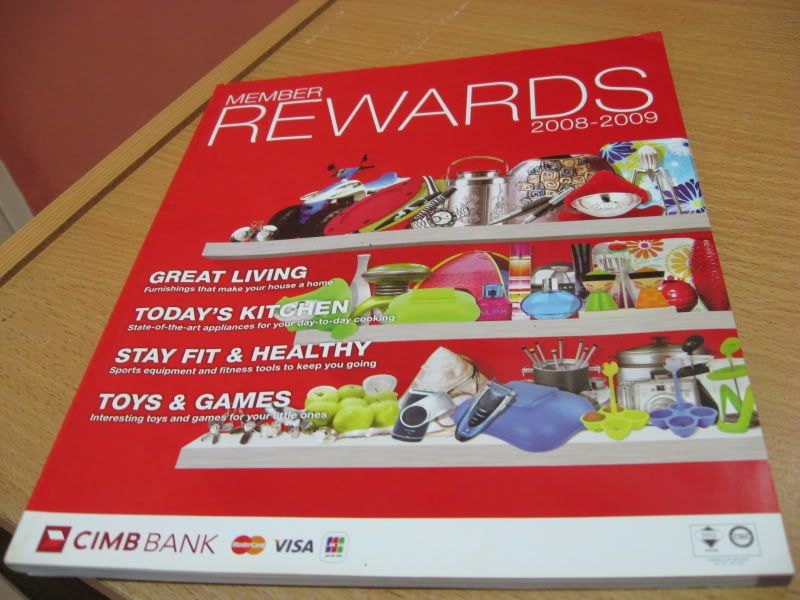

Catalog of Rewards

I must salute CIMB for coming up with a 150 pages catalog of things I can exchange for my credit cards. The catalog ranges from household things to electronic to vouchers to fitness tools to toys and many more. It is suited for everybody. Somehow they got it right. Not only that, with a minimum of 3000 points you can get something.If you do not have sufficient points, you can opt to go with special buy, paying cash with minimum points. I kind of like this idea because I can buy stuff at discounted rates. Do check the price properly, it may not be the best price for some items.

I have already identified some items I would exchange for. Looks like I will make my credit cards worked harder. 😛

-

Time For A Change

After being loyal to my credit card bank for more than 10 years, it is time to change. I found that my current credit card’s reward is not very attractive and service is deteriorating. Imagine after 3 years using my card, magnetic strip coming off and many calls to the service desk, just to get them to renew the card without the change of account number. I gave up and did no transaction on the card, then finally the approved the change.

I was surveying the market to see which credit card that will meet my needs. Recently I found one from CIMB, it is free for life with no condition and no administration fees whatsoever. I was really surprise and ask the agent a few times. Not only that, it is also a discount card for many places like Guardian, MPH, World of Cartoon and others. Lastly their reward point’s book is as thick as the Ikea magazine. Of coz the number of points collected is not a small number. It is alright because there is a variety.

I am glad they have a road show in Queensbay mall where I sign up for a Platinum Free for life card. The agent gave me a Swiss knife, a multipurpose torch and a huge umbrella. Good deal eh?! I cannot wait for the card to arrive at my mail box with the catalog and the discount outlets book.

-

Credit Cards Survey

I was surfing around to survey some credit cards out there. I have decided to change my credit card after 12 years of loyalty. I stayed with the bank because of their good service. However I found that their service has been deteriorating and it has the worst gift reward ever.

Anyway I saw this when I was surfing the bank website, it is really funny. The tag line is “For entrepreneur whose office is in the world” Anyone’s office in the planet or moon? It doesn’t protray the idea of exclusiveness. Mind you, it is a Platinum Business Card.

Jokes aside, so what are the good credit cards out there? It is funny, previously when I was not looking for a credit card, I see so many promoters everywhere. I used to walk like driving a car in an arcade trying to avoid them. Now I don’t see any of them. How sad, I was hoping to get some free gifts and goodies.

I heard that my friend used to sign up at every booth. He gets free goodies on the spot. However he didn’t received any credit cards, it must be an administrative bug. There he goes again and sigh up for the second or third round. I bet he got a whole lot of freebies in his home.

Today I heard that certain banks are giving no expiry dates on the bonus points of the credit cards. Anyone know whether CIMB credit cards bonus points expiry date? 1 year? 3 years? I kind of like the CIMB gift reward. I need to do more survey.

-

EPF Dilemma

The govt announced that we can reduce contribution from 8% to 11%. With this announcement, I am sure you heard quite a lot of rumors. I shall not anymore oil into the fire.

Last week, I received my company memo that it will be a default 8% contribution. If anyone wants to remain at 11%, we need to sign a form.

Now, the decision, should I sign or not? I don’t think the extra 3% is going to make a difference for me. You may say I can invest the 3% elsewhere. The question is whether the investment can measure up to the dividend given by EPF. Now fixed deposit interest rate is also lowered. I wondered what % dividend we will get from EPF this year. Any rumors?

I bet most of the younger generation will spend the extra 3% which is not good for their future. It means less money when they retired. Older generation will be wiser to keep the 3% in EPF. By the way, I saw a long list of signatures.

Should I sign or not?

-

How Many Times Do I Need To Cancel?

Last year I cancelled my supplementary UOB credit card because I have no use for it and it cost RM30 for admin fee. When they gave it to me, it was free. Somehow along the years, they added the RM30 policy but didn’t bother to inform the customer.

Anyway, to avoid any nightmares, I cancelled it. After I cancel it, it was deleted from the online system. Everything was fine until this year, it appeared again on my online system. Initially I wasn’t aware of it when I called the credit card helpline for another issue, they asked me whether I had any supplementary. I said no and she said yes. Hrmm…I told her I cancelled it last year.

What made me really frustrated was the officer asked me to submit another cancellation form? I told her no and why should I? I already did 1 year ago. I am not going to submit any documentation every year to cancel the stupid card. They told me that they didn’t receive my cancellation form. I bet they must have lost it.

I heard so many cases of bank making it difficult for customer to cancel the credit card. It is so unprofessional of them. Next time, I will charge them admin fee for asking me to submit a cancellation form. What should I charged? RM30 for 1 cancellation form.

Next time you sign up for a credit card, ensure the bank provide a easy way to cancel the card!

-

Charged For No Reason

How many of you check your saving accounts statement monthly? Few weeks ago, I checked my statement and saw my bank HSBC charged a fee of RM5 for month of Aug and Sep. I was really surprised because for more than 8 years I was with them, there was no fee whatsoever.

I called their helpline and when you need them, no one picked up the phone. I tried twice but failed to get someone to talk to me. I went to their website and left a feedback. A customer service officer emailed me and called me. She told me that she will investigate.

The thing is when they offered the account, they didn’t tell me there was a fee attached to it. The account was offered to my husband company for employees for salary deposit. No fees were mentioned. Anyway, I didn’t want to argue with them and requested for the refund for RM10 they took from my account. I will in turn close the account for good.

I was frustrated that they charge us without any notification. I will never open an account with RM5 monthly. It is day light robbery!

Do check your statement frequently to check for unknown charges.

-

Ripple Effect

Yesterday when the announcement of the rise of petrol price from RM1.90 to RM2.70, everyone wanted to pump petrol before it happens. Yes, it will save them RM20-RM30 if they can get to the petrol station. It caused havoc everywhere, cars queues were 1 km long. You probably have to jam for an hour or more to pump.

Thank you all for SMS-ing me, emailing me or called me. However it was really a waste of time, energy and petrol for me to queue for 1 hour or more to get that savings.

Today, guess where was congested? Our own office cafeteria, it seems that everyone decided to eat in. The queue to the counter to get food was long but not longer than the petrol Q. Hehehehe. The cashier counter was as long.

The next thing that goes up will be electricity, food, etc. Let’s hope my year end increment will go up too. Life is so meaningless. Don’t you think?

-

EPF Loan Reduction Process

I am impressed with KWSP as it has speed things up a lot compare to many years ago. I got my cheque like 2 weeks after submitting my documentation. It should be fairly fast if all your documents are in tact.

If you want to speed up the process of getting all the documents without hassle, you can request the bank where you get the loan from to assist you. They charge a nominal fee. For HSBC, it is RM50.

Papers required for loan reduction are:

- Photocopy of your myKad

- A certified copy of your S&P

- A certified copy of your bank loan agreement

- A letter from your bank confirming the latest outstanding balance of housing loan

- according to the preset format. It is better to request a projection of 3 months.

- Deed of Title (11A/B) or Deed of Assignment.

- All Housing Loan Redemption Letters if you did refinancing previously.

- KWSP 9C Form

The KWSP website is very informative and you can find most of the forms there.

-

Cashing US Cheque

I sold some shares a month ago and the broker sent me a US cheque. As you know there are bank fees involved in cashing US cheque. The cheque needs to send back to the US bank for verification. The bank told me that they charged 0.1% of the amount on the cheque, minimum RM10. Stamp duty is RM0.15. I went to CIMB to cash out my cheque. It took around 4 weeks to cash out. I heard Citibank giving a lower rate if you have an account with them. Not sure how true.

If you are selling shares amounting to greater than US10K, it is better to use wire transfer as the cost of that is US25. Save the hassle and faster turn around time to get your money.

More info

myHotel Review

- Malaysia:

- Hard Rock Hotel Penang

- Penang Golden Sands

- Genting Resort World Malaysia

- Berjaya Langkawi Resort

- Singapore:

- Grand Hyatt Hotel In Singapore

- Singapore Royal Plaza

- Hong Kong

- Hong Kong Hollywood Disneyland Hotel

- US:

- Hyatt Summerfield Hotel in Colorado Springs

- Hotel Carlton San Francisco

- Santa Rosa Hilton Hotel

- Hyatt Vineyard Creek Hotel & Spa Santa Rosa

recent

- Penang Bon Odori 2014

- Garden Shopping

- Health Tips

- Maker vs Marker

- 10 More Life Hacks

- Benefits of Cucumber

- Chinese New Year 2014 Dishes

- Loom

- Curry Leaves

- Of First Fruit & Flower

Archives

- July 2014 (1)

- June 2014 (1)

- April 2014 (1)

- March 2014 (2)

- February 2014 (2)

- January 2014 (3)

- December 2013 (1)

- November 2013 (2)

- October 2013 (2)

- September 2013 (1)

- August 2013 (2)

- July 2013 (5)

- June 2013 (4)

- May 2013 (10)

- April 2013 (1)

- March 2013 (5)

- February 2013 (3)

- January 2013 (4)

- December 2012 (3)

- November 2012 (3)

- October 2012 (6)

- September 2012 (4)

- August 2012 (3)

- July 2012 (6)

- June 2012 (2)

- May 2012 (3)

- April 2012 (3)

- March 2012 (1)

- February 2012 (2)

- January 2012 (2)

- December 2011 (4)

- October 2011 (4)

- September 2011 (7)

- August 2011 (2)

- July 2011 (1)

- June 2011 (3)

- May 2011 (1)

- April 2011 (1)

- March 2011 (3)

- February 2011 (4)

- January 2011 (1)

- December 2010 (2)

- November 2010 (2)

- October 2010 (7)

- September 2010 (5)

- August 2010 (8)

- July 2010 (3)

- June 2010 (5)

- May 2010 (7)

- April 2010 (9)

- March 2010 (10)

- February 2010 (5)

- January 2010 (6)

- December 2009 (6)

- November 2009 (6)

- October 2009 (6)

- September 2009 (7)

- August 2009 (11)

- July 2009 (8)

- June 2009 (7)

- May 2009 (9)

- April 2009 (7)

- March 2009 (8)

- February 2009 (9)

- January 2009 (6)

- December 2008 (11)

- November 2008 (7)

- October 2008 (9)

- September 2008 (10)

- August 2008 (11)

- July 2008 (11)

- June 2008 (10)

- May 2008 (14)

- April 2008 (16)

- March 2008 (13)

- February 2008 (11)

- January 2008 (10)

- December 2007 (6)

- November 2007 (21)

- October 2007 (11)

- September 2007 (10)

- August 2007 (14)

- July 2007 (3)

- June 2007 (3)

- May 2007 (3)

- April 2007 (6)

- March 2007 (10)

- February 2007 (4)

- January 2007 (11)

- December 2006 (4)

- November 2006 (5)

- October 2006 (7)

- September 2006 (5)

- August 2006 (1)

- July 2006 (1)

- June 2006 (6)

- May 2006 (3)

- April 2006 (6)

- March 2006 (5)

- February 2006 (1)

- January 2006 (3)

- December 2005 (2)

- November 2005 (5)

- October 2005 (7)

- September 2005 (12)

- August 2005 (4)

- July 2005 (2)

- June 2005 (2)

- May 2005 (1)

- April 2005 (4)

Categories

- Advertlets

- Auction

- Award

- Baby

- Balloon

- Blogs

- Book

- Breastfeeding

- Business

- Car

- Charity

- Children

- Christianity

- Coach

- Collection

- Craft

- CStory

- Deco

- Design

- Dream

- Driving

- Economy

- English

- Entertainment

- Environment

- EPF

- Event

- Experience

- Finances

- Food

- Friends

- Furniture

- Game

- Garden

- Garden Tips

- Gift

- Greed

- Handphone

- Hangbag

- Health

- Hobby

- Hotel

- Household Tips

- Humor

- Information

- Insurance

- Internet

- Investment

- iPhone

- IT

- Kuala Lumpur

- Langkawi

- LB

- Living

- Malaysia

- Management

- Movie

- Music

- Myself

- Nature

- News

- Parenting

- Penang

- Photobook

- Playground

- PR

- ProductReview

- Rant

- RealityShow

- Recall

- Rental

- Reward

- Scam

- School

- Science

- Search Engine

- Service

- Shares

- Shopping

- Singapore

- Skill

- Special Day Event

- Stamps

- Sushi

- Tag

- Tax

- Technology

- Theme Park

- Tips

- Toys

- Travel

- Uncategorized

- US

- Video

- Vitamins

- Web Host

- Will

- Work

feeds

![]()

Copyright

Copyright © 2007 by Parkbay. All rights reserved.